Video-Course: Region dos, Component cuatro: The latest Subprime Home loan Crisis: Grounds and you may Classes Read

On late 2000′s, a series of fiscal conditions arrived together result in a primary downturn in a residential property and home loan fund segments. It bursting of your a home ripple composed a ripple impression from the cost savings that’s now also known as the subprime mortgage crisis.

Video-Course: User Protection and you can Equivalent Chance in the A property Credit-Component step three of 5

The brand new affects of your own crisis had been around the globe during the level. Within this module, we are going to consider just what prominent home loan techniques about Joined States lead to the crisis and just how the federal government taken care of immediately new failure. We’re going to focus on a few of the most popular issues one to shared towards the best financial pullback as High Anxiety of one’s 1930s. Just after investigating the causes of the economic recession, brand new discussion after that converts in order to how Congress answered into the Dodd-Frank Wall surface Highway Reform and you can Individual Defense Act.

By 2007, real estate markets were over-over loaded with over-priced land becoming bought of the people who posed large borrowing from the bank dangers. Lenders provided aside expensive mortgage loans throughout a bona-fide home boom you to some one seemed to imagine manage last forever. Since a residential property viewpoints tucked, most of these mortgages amounted in order to more the newest homes’ complete philosophy. Many home owners located themselves struggling to manage the monthly mortgage payments, as well as you will not re-finance or promote because of plummeting real estate values. Many Us citizens who had been behind on the mortgage loans had no way of to prevent default. That it harrowing consolidation resulted in online payday loans North Dakota no credit check individuals defaulting on their home loans for the list wide variety, which have nearly four billion house foreclosed on between 2008 and you may 2014. Millions of family members had been leftover homeless. But exactly how did this all happen?

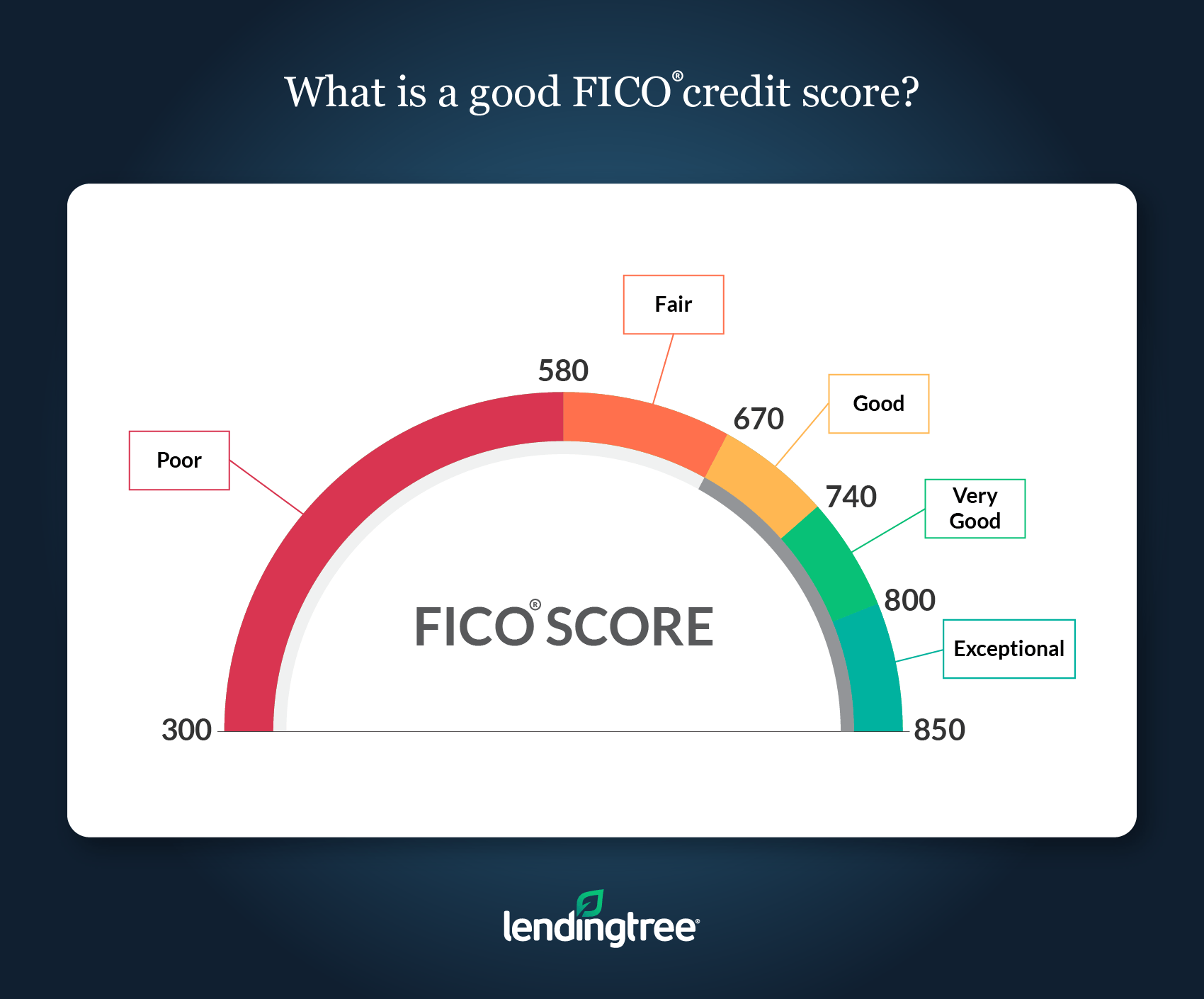

The financial collapse of 2007 to 2009 is commonly referred to as the subprime mortgage crisis because this lending practice is considered the main trigger of the collapse. The Federal Reserve defines subprime mortgage loans as loans made to borrowers who are perceived to have high credit risk, often because they lack a strong credit history or have other characteristics that are associated with high probabilities of default. The subprime qualifier thus refers to the borrower’s credit rating, not the loan itself. In other words, subprime lending practices extended mortgage loans to people who would have typically been denied credit under more conservative financial policies.

Subprime loans become increasing in popularity on middle-1990′s. Within the 1994, complete subprime mortgage loans approved in america amounted to help you $35 mil. By 1999, that amount have more quadrupled to $160 billion. This trend continued adopting the change of the millennium, and you may lenders have been in the future supplying a huge selection of billions of cash into the risky money. For the 2006, a single 12 months till the overall economy theoretically struck, loan providers granted $600 million in subprime mortgages.

Around once in Western background, they turned well-known having banking institutions issuing mortgages to offer them to high investment banks, who does resell otherwise exchange many mortgage loans by creating immense securities comprised of home loan passion. It turned popular, and still is normal, having financial institutions to help you topic mortgage loans and turnaround and sell people mortgages to other finance companies otherwise investment financial institutions within months.

… all joint in order to make a feeling where and you can finance companies had all added bonus so you can flake out the latest certificates and requirements for mortgage loans.

Within ecosystem, it is perhaps unsurprising you to definitely financial institutions found by themselves providing much more much more mortgage loans to the people who have been less and less accredited. Besides was indeed these loans awarded in order to risky individuals, up to seventy percent of your apps for these fund may have contains not the case informationmonly, individuals will make untrue comments about money otherwise would untrue earnings verification data. Because of lax data procedures therefore the standard loose borrowing from the bank conditions, this type of misrepresentations tend to went unnoticed.