bad credit personal loans North Dakota

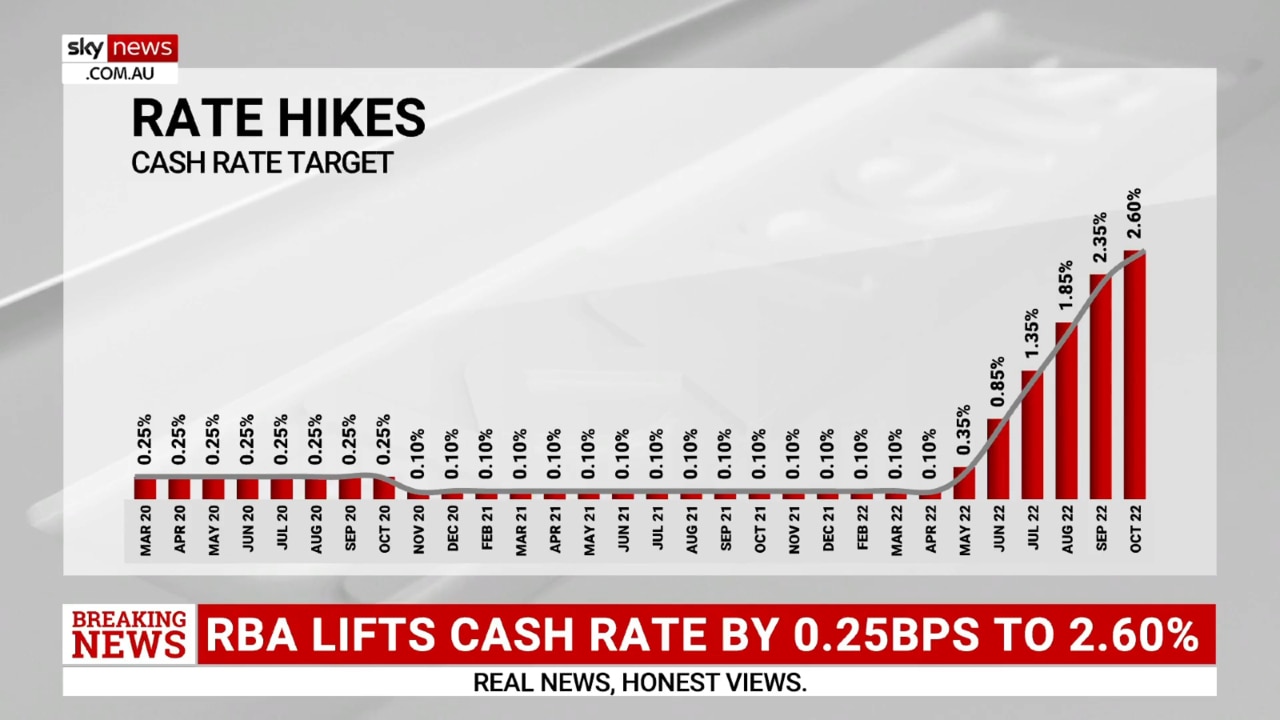

Over the years lowest, pandemic-time mortgage pricing possess considering increase so you can a size lock-inside the of sorts certainly one of home owners anybody very linked with its low cost these are typically unwilling to buy yet another property in the prevalent can cost you. Because they look inside their pumps, what is actually a lender to accomplish?

In the Pennymac, the obvious choice to the standoff are a house equity loan colloquially known from the company in given that an excellent closed-stop next circulated just last year. It’s a different sign of the times as the loan providers be more innovative in their unit products in order to entice business in the midst of an excellent downshifted markets.

Home loan Top-notch The usa talked to Scott Links (pictured), elderly dealing with director, user lead financing, for additional info on this new growing appeal of this product an excellent nothing over a-year while the their rollout.

We have yes viewed a very deep change, Links advised MPA through the a telephone interviews. Obviously, there is no price and you can label refinancing taking place at all. That’s effortlessly gone. Individuals has 3% mortgage loans or reduced 4s otherwise highest 2s, and often it does not make sense to allow them to refinance their earliest mortgage loans to locate cash-out because their the fresh rate was will be six.5% so you can seven.5% within this sector.

Closed-avoid next towards the save yourself

Enter the finalized-avoid second. It is really not an excellent HELOC, Links insisted. “It’s a house collateral mortgage second home loan. You have made a lump sum. When you want $75,000, you get $75,000. We see most of all of our consumers explore their money having statement combination, home improvements or any other means.

The product is apparently a knock of these guarding the lowest prices cost so reasonable these include unlikely to be noticed again. You realize it’s been a very popular product for us, Bridges told you. It has got performed better; the user consult is good.

Since the the discharge from inside the , consumers appear to be utilising the finalized-prevent second providing judiciously: We have an optimum LTV out-of 85%, but we see a number of our very own consumers maybe not supposed one higher and you can borrowing from the bank 65% otherwise 70% whilst still being leaving specific equity area, which is higher.

The merchandise could have been perfect for LOs also, Links detailed: It is invited the loan officers to remain at capacity and sustain active, the guy told you. If we didn’t have an additional financial unit, it might be a more challenging market for united states.

Issues arise while the America’s obligations stream passes $step 1 trillion

An additional indication of the times, the merchandise features came up at once off listing-setting unsecured debt. According to the New york Government Set-aside Financial, balances exceeded $step 1 trillion for the first time that have bank card stability rising because of the $forty-five million to $step one.03 trillion in the second one-fourth.

It will be the very first time at this moment Americans’ loans load might have been you to highest, and is low-home loan. So yeah, we have been in an inflationary sector and you can customers of security can increase their money flow, yes if they are consolidating financial obligation.

Requested set up a baseline attesting for the signed-end second item’s triumph, Links given: We have locked because the beginning north away from $750 million.

An additional benefit into the product is your day feature to own fees is at the new discernment of one’s individual, the guy noted. It isn’t a HELOC, such as for example We said, its a lump sum payment shipping. HELOCs work with some people. We don’t promote HELOCs. I perform for instance the house security financing in the place of the latest HELOC just like the it is a totally amortized obligations. HELOC is kind of an unbarred-concluded bit of borrowing it doesn’t fully amortize. You will find conditions having ten, fifteen, 20 and you can 30 years, and so the individual can decide its payback schedule once they want a lesser fee, they may be able features a longer time; if they wanted a high commission and wish to shell out it from more quickly, they’re able to like a minimum name regarding ten years.

Really consumers seem to be breaking the difference: We see the majority of our customers demand 20-season name, Bridges told you.

From the six months in the past, Pennymac circulated an alternative unit symbolic of one’s minutes a temporary buydown device available for pick funds merely.

Let’s say prices today are 6.5%, Links posited. The buydown is actually a-1-0 buydown, therefore, the first 12 months regarding repayment your own rates would-be 5.5% 1% less than industry. You pay a little fee attain you to, although advantage of the newest buydown exceeds the fee however, or you wouldn’t get it done. We find one is extremely prominent. Because i rolled one to aside, we’ve locked northern out-of a quarter-mil during the buydown for sale purchases.

The guy informed me the newest notice subsequent: When you look at the market similar to this which is most unstable, it offers prevalent focus as if you are doing a good buydown financing having a year, the rate could be top within the per year and also you you will indeed refi at the time. You would have the down rate into the first 12 months and you may this may be carry out return to the product quality speed of these go out.

An alternative in addition to ‘s the unit does not have brand new costs in the a great HELOC, Links additional: An excellent HELOC usually has a minimum commission framework and other charge associated with using it, Links said. There’s absolutely no annual costs in regards to our domestic equity mortgage. It is simply practical loan costs within closure, identity, etc.

An additional reaction to the fresh new unstable business, Pennymac just last year launched the Lock & Store merchandise that permits customers to frost home loan cost because they still store a separate equipment driven by the most recent volatile sector.

Using Lock & Shop, people can decide certainly one of about three lock words: a good 60-, 75- otherwise 90-go out secure, providing customers 29, forty five and you can 60 days to shop, correspondingly. When you look at the a previous interviews, Bridges said the business grabbed notice of the sector within the establishing the merchandise as they saw cost carried on to rise as the Given looks to fight out of inflation. We set up an effective Secure & Store tool where you could protect the rates now to own to ninety days whilst you shop for a property, which will secure within the present rate, Bridges told you.

Pennymac is certainly going to the disperse in the modern uncharted waters, however with an array of situations to store they afloat. Look, it’s not a simple markets, Links accepted. You have to be nimble and you need to has actually a beneficial circumstances, diversity to own customers, and particularly items that offer discounts inside the a top markets.

Want to make the inbox flourish which have home loan-concentrated information content? Rating exclusive interviews, cracking reports, trade events on your own email, and constantly function as the first to understand from the signing up for our Free everyday newsletter